- The U.S. CoreLogic HPI was up 5.4% compared to April 2019, with gains in all states

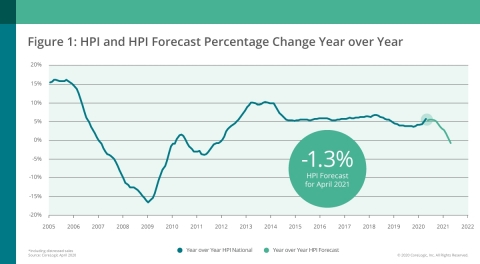

- The HPI Forecast predicts the U.S. index will fall 1.3% from April 2020 to April 2021—after nine years of annual price gains, 2021 is forecasted to post an annual price decline

- CoreLogic Market Risk Indicators shows areas hit by downturns in tourism and oil and gas will experience largest home price declines

IRVINE, Calif. — (BUSINESS WIRE) — June 2, 2020 — CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released the CoreLogic Home Price Index (HPI™) and HPI Forecast™ for April 2020. Nationally, home prices increased by 5.4%, compared with April 2019. Home prices increased 1.4% in April 2020 compared with March of this year.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20200602005254/en/

CoreLogic National Home Price Change and Forecast; April 2020 (Graphic: Business Wire)

The home price acceleration in the April HPI was supported by increased homes sales in the first quarter of the year. Home price growth is expected to decelerate somewhat in May, with the CoreLogic HPI Forecast calling for a month-over-month increase of 0.3% compared with April 2020. Looking ahead, the CoreLogic HPI Forecast predicts an annual price decline of 1.3% from April 2020 to April 2021. In 2021, home prices are expected to decline for the first time in more than nine years.

Home-purchase activity slowed over March and April compared to last year as shelter-in-place orders, and an unprecedented spike in unemployment, dented home-buying activity fueled by millennials. Nationally, the for-sale inventory of entry-level homes plummeted on average 25% in April. Should this trend continue, we may see an adverse effect on home sales in the near term.

“The very low inventory of homes for sale, coupled with homebuyers’ spur of record-low mortgage rates, will likely continue to support home price growth during the spring,” said Dr. Frank Nothaft, chief economist at CoreLogic. “If unemployment remains elevated in early 2021, then we can expect home prices to soften. Our forecast has home prices down in 12 months across 41 states.”

The Market Risk Indicator (MRI), a monthly update of the overall health of housing markets across the country, predicts a very high probability (above 60%) of a decline in home prices in Prescott, Arizona; Huntington, West Virginia; Cape Coral-Fort Myers, Florida; and College Station-Bryan, Texas, over the next 12 months. It also predicts a moderate probability of a price decline (40-60%) in North Port-Sarasota-Bradenton, Florida. Huntington, West Virginia, was hit particularly hard by the recent downturn in the oil and gas industry. Typical vacation spots, like Cape Coral-Fort Myers and North Port-Sarasota-Bradenton in Florida, as well as Prescott, Arizona, are also expected to experience a decline in home property value as visitors stay home and vacation rentals are sold.

According to the CoreLogic Market Condition Indicators (MCI), an analysis of housing values in the country’s 50 largest metropolitan areas based on housing stock, 40% of metropolitan areas had an overvalued housing market in April 2020, while 18% were undervalued and 42% were at value. The HPI Forecast continues to show the inequality of home prices across metros. In overvalued markets like Las Vegas and Miami, where the local tourism economy took a hit due to COVID-19, home prices are expected to decline by 7.2% and 4.4%, respectively, by April 2021.

The nationwide HPI of single-family attached units (condos, duplexes), the more affordable housing option, increased by 4.3% year over year in April 2020, whereas the single-family detached increased by 5.7% year over year. This is indicative of home buyers continuing to take advantage of low rates — and therefore lower monthly payments — to purchase larger detached properties that may have otherwise been out of their price range.

The Philadelphia metro area, where New York City residents are reported to be relocating in the wake of the COVID-19 outbreak, and likely in search of more space and privacy, experienced the largest year-over-year increase in prices of single-family detached home by 10.6%. Alternatively, Houston experienced one of the lowest year-over-year price increases of 0.7% in single-family attached homes as low-income jobs vanished with the oil and gas collapse.

“Tight supply and pent-up demand, particularly among millennials, provides optimism for a bounce-back in the housing market purchase activity and home prices over the medium term,” said Frank Martell, president and CEO of CoreLogic. “The next 12 to 18 months are going to be very tough times for the broader economy. As employment and economic activity begin to pick up, as it will surely do, we expect housing to be a driver in a national recovery.”

The next CoreLogic HPI press release, featuring May 2020 data, will be issued on July 7 at 8:00 a.m. ET.

Methodology

The CoreLogic HPI™ is built on industry-leading public record, servicing and securities real-estate databases and incorporates more than 40 years of repeat-sales transactions for analyzing home price trends. Generally released on the first Tuesday of each month with an average five-week lag, the CoreLogic HPI is designed to provide an early indication of home price trends by market segment and for the “Single-Family Combined” tier, representing the most comprehensive set of properties, including all sales for single-family attached and single-family detached properties. The indices are fully revised with each release and employ techniques to signal turning points sooner. The CoreLogic HPI provides measures for multiple market segments, referred to as tiers, based on property type, price, time between sales, loan type (conforming vs. non-conforming) and distressed sales. Broad national coverage is available from the national level down to ZIP Code, including non-disclosure states.

CoreLogic HPI Forecasts™ are based on a two-stage, error-correction econometric model that combines the equilibrium home price—as a function of real disposable income per capita—with short-run fluctuations caused by market momentum, mean-reversion, and exogenous economic shocks like changes in the unemployment rate. With a 30-year forecast horizon, CoreLogic HPI Forecasts project CoreLogic HPI levels for two tiers — “Single-Family Combined” (both attached and detached) and “Single-Family Combined Excluding Distressed Sales.” As a companion to the CoreLogic HPI Forecasts, Stress-Testing Scenarios align with Comprehensive Capital Analysis and Review (CCAR) national scenarios to project five years of home prices under baseline, adverse and severely adverse scenarios at state, metropolitan areas and ZIP Code levels. The forecast accuracy represents a 95% statistical confidence interval with a +/- 2% margin of error for the index.

About Market Risk Indicator

Market Risk Indicators are a subscription-based analytics solution that provide monthly updates on the overall “health” of housing markets across the country. CoreLogic data scientists combine world-class analytics with detailed economic and housing data to help determine the likelihood of a housing bubble burst in 392 major metros and all 50 states. Market Risk Indicators is a multi-phase regression model that provides a probability score (from 1 to 100) on the likelihood of two scenarios per metro: a >10% price reduction and a ≤ 10% price reduction. The higher the score, the higher the risk of a price reduction.

About the Market Condition Indicators

As part of the CoreLogic HPI and HPI Forecasts offerings, Market Condition Indicators are available for all metropolitan areas and identify individual markets as “overvalued,” “at value,” or “undervalued.” These indicators are derived from the long-term fundamental values, which are a function of real disposable income per capita. Markets are labeled as overvalued if the current home price indexes exceed their long-term values by greater than 10%, and undervalued where the long-term values exceed the index levels by greater than 10%.

Source: CoreLogic

The data provided are for use only by the primary recipient or the primary recipient's publication or broadcast. This data may not be resold, republished or licensed to any other source, including publications and sources owned by the primary recipient’s parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data are illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Allyse Sanchez at

corelogic@ink-co.com . Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. The data are compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

Animation, 3D Art and 3D Models")